Timeshare Mortgage Interest Rates: Why They're So High — and What It Means for Your Exit

Timeshare Mortgage Interest Rates: Why They're So High — and What It Means for Your Exit

When timeshare salespeople quote you a monthly payment instead of a total price, there's a reason. The monthly number sounds manageable. The interest rate — and the total amount you'll actually pay — does not.

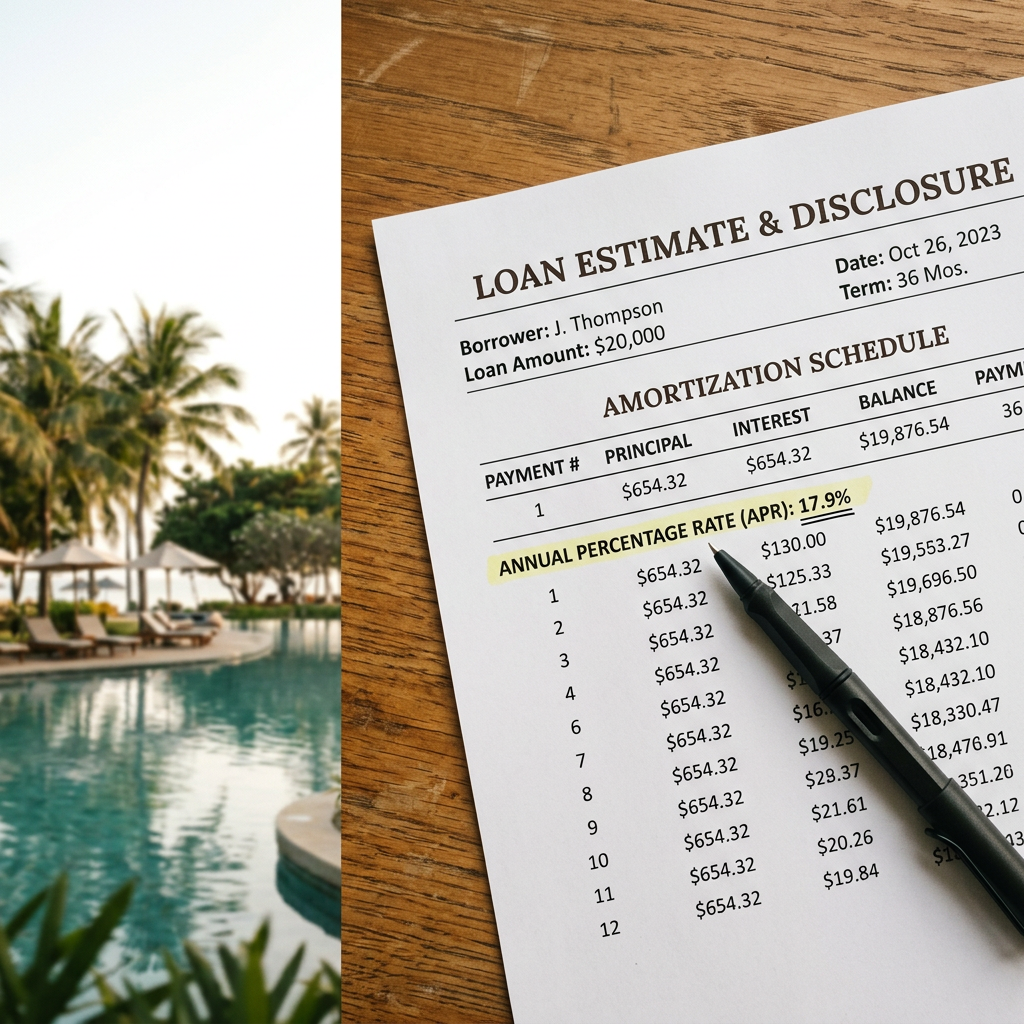

Timeshare developer financing routinely runs between 14% and 20% APR. On a $20,000 timeshare purchase financed over ten years, that's not $20,000 out of pocket. It's closer to $38,000 — before a single maintenance fee.

This post covers how timeshare loans work, why the rates are structured the way they are, what you're actually paying over the life of the loan, and — most importantly — how an outstanding balance changes your options when you want out.

Why Are Timeshare Interest Rates So Much Higher Than a Mortgage?

Timeshare loans are not mortgages. This is the first thing most buyers don't understand when they sign at the sales table.

A traditional mortgage is secured by real property — your home. If you stop paying, the lender can foreclose on an asset with market value and recover their money. That security is what allows banks to offer 6–8% rates on 30-year home loans.

A timeshare is a different animal. Even when it's structured as a "deeded interest" in real property, the secondary market for timeshares is essentially nonexistent. Owners list their weeks on platforms like RedWeek or eBay for $1 and still can't give them away. This means the developer's loan is secured by an asset with near-zero resale value.

To compensate for that risk, developers charge rates that more closely resemble consumer credit or personal loan products — not real estate financing. Wyndham Financial Services, Marriott Vacations Worldwide's lending arm, and Bluegreen's in-house financing have all historically offered rates in the 14–20% range depending on credit profile and purchase amount. Some smaller independent resort developers go higher.

The Truth in Lending Act (TILA), enforced by the Consumer Financial Protection Bureau, requires that APR and total finance charges be disclosed before signing. In practice, that disclosure is buried in a thick contract stack that buyers are rushed through — often during high-pressure sales presentations that run four to six hours and end with a closing offer that expires "tonight only."

What Does a Timeshare Loan Actually Cost Over Time?

Let's use a concrete example with conservative numbers.

Purchase price: $22,000 (near the national average for a new timeshare week) Down payment: $2,200 (10%) Financed amount: $19,800 APR: 16.9% Term: 10 years (120 months)

At those terms, your monthly payment is approximately $338. Over 120 months, you'll pay roughly $40,560 in total — meaning $20,760 goes to interest alone on a $19,800 loan.

Add in annual maintenance fees averaging $1,200–$1,500 per year (and rising 3–5% annually per American Resort Development Association data), and the ten-year all-in cost of that timeshare approaches $55,000–$60,000.

None of that money builds equity. Timeshares do not appreciate. They cannot be refinanced through a conventional lender. And they cannot be easily sold.

This is the core financial trap — not just the purchase, but the compounding of high-interest developer financing layered on top of perpetual annual fees and periodic special assessments.

Can You Refinance a Timeshare Loan?

Rarely, and with significant difficulty.

Unlike a home mortgage, a timeshare loan cannot be refinanced through a bank, credit union, or conventional lender because no lender will accept the timeshare as collateral. The asset doesn't have a functional market value.

Some owners have refinanced by taking out a personal loan or home equity line of credit (HELOC) at a lower rate and using those proceeds to pay off the developer loan. This can reduce the interest burden, but it shifts the debt onto your primary home — which creates new risk. If you later pursue an exit and stop paying the now-paid-off developer, you're not in the clear: you've simply moved the debt to a secured product attached to your house.

A few credit unions — most notably USAA members who purchased at military-adjacent resorts — have historically offered timeshare-specific refinancing products, but these are rare and not broadly available.

The better use of a HELOC or personal loan is not to refinance and stay — it's to pay off the developer balance and then pursue a formal exit, since having no outstanding mortgage is typically a prerequisite for deed-back programs and many third-party exit processes.

How Does an Outstanding Timeshare Loan Affect Your Exit Options?

This is where the loan issue becomes critical — and where most owners get stuck.

Deed-back programs require a paid-off loan. The Wyndham Ovation Program, Marriott's Abound Exit path, and virtually every other resort-offered voluntary surrender requires that the timeshare carry no outstanding mortgage. The resort won't absorb a liability-generating asset that also has a lien on it from their own financing arm. If you're still paying off your developer loan, you are not eligible.

Third-party exit companies work around the loan differently. Legitimate exit companies don't require a paid-off mortgage as a condition of starting the process, but the loan complicates the timeline. In cases built around misrepresentation or FTC Holder Rule violations — which can name the lender as a co-party when the lender is the same entity as or affiliated with the developer — the loan itself can become part of the dispute. This is a stronger case for owners who financed directly through Wyndham Financial Services or Marriott Vacations Worldwide's lending affiliate, because the same corporation sold and financed the contract.

Stopping payments affects both your credit and your loan separately. If you stop paying maintenance fees, the resort reports delinquency and can pursue collections or foreclosure on the timeshare interest. If you stop paying the developer loan, the lender reports to credit bureaus and can pursue the loan balance independently — sometimes selling it to a third-party collector operating under the Fair Debt Collection Practices Act. These are two separate creditors and two separate delinquency tracks.

Many owners discover this the hard way when they assume stopping maintenance fees is the same as stopping their loan payment.

For a full picture of what payment stoppage triggers, see our guide on what happens when you stop paying timeshare maintenance fees.

What Is the FTC Holder Rule and Why Does It Matter for Timeshare Loans?

The FTC Holder Rule (16 CFR Part 433) is a federal regulation that preserves a buyer's right to assert claims against a creditor when the creditor is connected to the seller. In plain terms: if you were defrauded by a timeshare developer and that same developer (or an affiliated entity) financed your purchase, you can assert that fraud as a defense against the lender.

This matters enormously in timeshare cases because the major developers are vertically integrated. When Wyndham sells you a contract and Wyndham Financial Services finances it, they are effectively the same organization. When Marriott Vacations Worldwide sells and finances, same situation. The Holder Rule means a timeshare attorney may be able to cancel both the contract and the associated loan in a single action — provided misrepresentation at the point of sale can be documented.

Not every timeshare owner was defrauded in a legally actionable way. But if you were promised rental income that never materialized, told the timeshare could be resold at profit, given false urgency around a "limited offer," or had material terms omitted from the verbal presentation, those are documented patterns in the FTC's timeshare enforcement history and can form the basis of a claim.

What If You Used a Credit Card or Personal Loan to Buy a Timeshare?

Some buyers — especially those who resisted developer financing at the table — paid with a personal loan, a credit card cash advance, or a GoodLeap or similar third-party product.

This changes the exit calculus in two important ways.

First, the Holder Rule still applies to affiliated third-party lenders in some cases, but the connection is harder to establish with truly independent credit. A Visa or Mastercard cash advance that funded a timeshare purchase does not typically give you recourse against the card issuer for the timeshare developer's misrepresentation — you'd need to pursue the developer directly.

Second, independent financing often carries lower rates than developer financing — sometimes significantly. If you used a personal loan at 8–10% instead of developer financing at 16–18%, your total loan cost is materially lower, though you're still stuck with the contract and the maintenance fees.

In either case, paying off the loan — through whatever means — typically opens the door to deed-back eligibility and simplifies exit negotiations with third-party exit firms.

Can You Dispute a Timeshare Loan Through Your State Attorney General?

Yes, and it's an underused option.

State attorneys general in Florida, Nevada, Tennessee, Missouri, and South Carolina — states with high concentrations of timeshare resorts — have active consumer protection divisions that handle timeshare complaints. The Florida Attorney General has brought enforcement actions against multiple exit companies and resort operators under Florida Statute § 721, which governs timeshare sales, disclosures, and cancellation rights.

Filing a complaint doesn't automatically cancel your contract or your loan. But it creates an official record, can trigger an investigation, and sometimes prompts the resort or lender to offer a settlement — particularly if they see the complaint as a precursor to a class action or regulatory action.

The Consumer Financial Protection Bureau also accepts complaints about timeshare loan servicing, payment disputes, and lender misrepresentation. Filing there creates a federal record that can support future legal action.

Frequently Asked Questions

What is the average APR on a timeshare loan from a developer? Developer timeshare financing typically runs between 14% and 20% APR, depending on creditworthiness and purchase amount. This is substantially higher than conventional mortgage rates because timeshares carry near-zero resale value and cannot be used as collateral by third-party lenders.

Can I refinance my timeshare loan through a bank? No traditional bank will refinance a timeshare loan because they won't accept the timeshare as collateral. Some owners use personal loans or HELOCs to pay off the developer balance — but shifting the debt to a home equity line carries its own risks and should only be done as part of a planned exit strategy.

Does paying off my timeshare loan mean I can exit? Paying off your loan makes you eligible for deed-back programs, which most resorts require as a condition of voluntary surrender. It also simplifies third-party exit negotiations. However, paying off the loan alone does not cancel the contract — you still own the timeshare and owe maintenance fees until a formal exit is completed.

What happens to my timeshare loan if I stop making payments? Nonpayment triggers credit reporting after 90–120 days and can result in the loan balance being sold to a third-party debt collector. This is independent of the resort's maintenance fee collections process — both run simultaneously. A timeshare loan default can appear on your credit report for seven years.

Is the FTC Holder Rule applicable to all timeshare loans? The FTC Holder Rule applies when the creditor is affiliated with or has an assigned relationship to the seller. It most cleanly applies to in-house developer financing (Wyndham Financial Services, Marriott's lending arm). It may not apply to independent third-party credit cards or unrelated lenders.

The Bottom Line

Timeshare developer financing is not a mortgage — it's closer to a high-rate personal loan secured by an asset nobody else will buy. The interest rates are high by design, the disclosure is buried, and the monthly payment framing at the sales table is intentional misdirection.

If you're still paying off your timeshare loan, you're not without options — but your path out is more complex than for owners who are mortgage-free. Understanding where your loan came from, who services it, and whether the Holder Rule applies is the first step to building a real exit strategy.

Get a free consultation to review your contract and financing situation →