Stop Paying Timeshare Maintenance Fees: What Actually Happens (And When It's a Bad Idea)

Stop Paying Timeshare Maintenance Fees: What Actually Happens (And When It's a Bad Idea)

The short answer: You can stop paying your timeshare maintenance fees, but it doesn't end the contract — it triggers a 6 to 18-month process of collection calls, credit damage of roughly 100–200 points, and (in states like Florida and Nevada) the possibility of a judgment against you for the unpaid balance. The contract itself stays alive until the developer forecloses or formally terminates it. For most owners, there are four legal alternatives that solve the maintenance fee problem without wrecking your credit. This post walks through what really happens if you stop, when it's the right call, and what to do instead.

If you're reading this, you've probably just opened your latest maintenance fee invoice. It's gone up again. The resort is impossible to book. You haven't used the timeshare in years. And you're done. The question isn't whether you want to stop paying — you already do. The question is whether stopping is actually going to solve the problem or just create a new one.

Here's the honest version of what happens next.

What Actually Happens When You Stop Paying

Stopping payment doesn't make a timeshare contract disappear. The contract is a legal document recorded with the county (for deeded timeshares) or held by the developer's membership database (for points-based contracts). Walking away from the payments triggers a sequence:

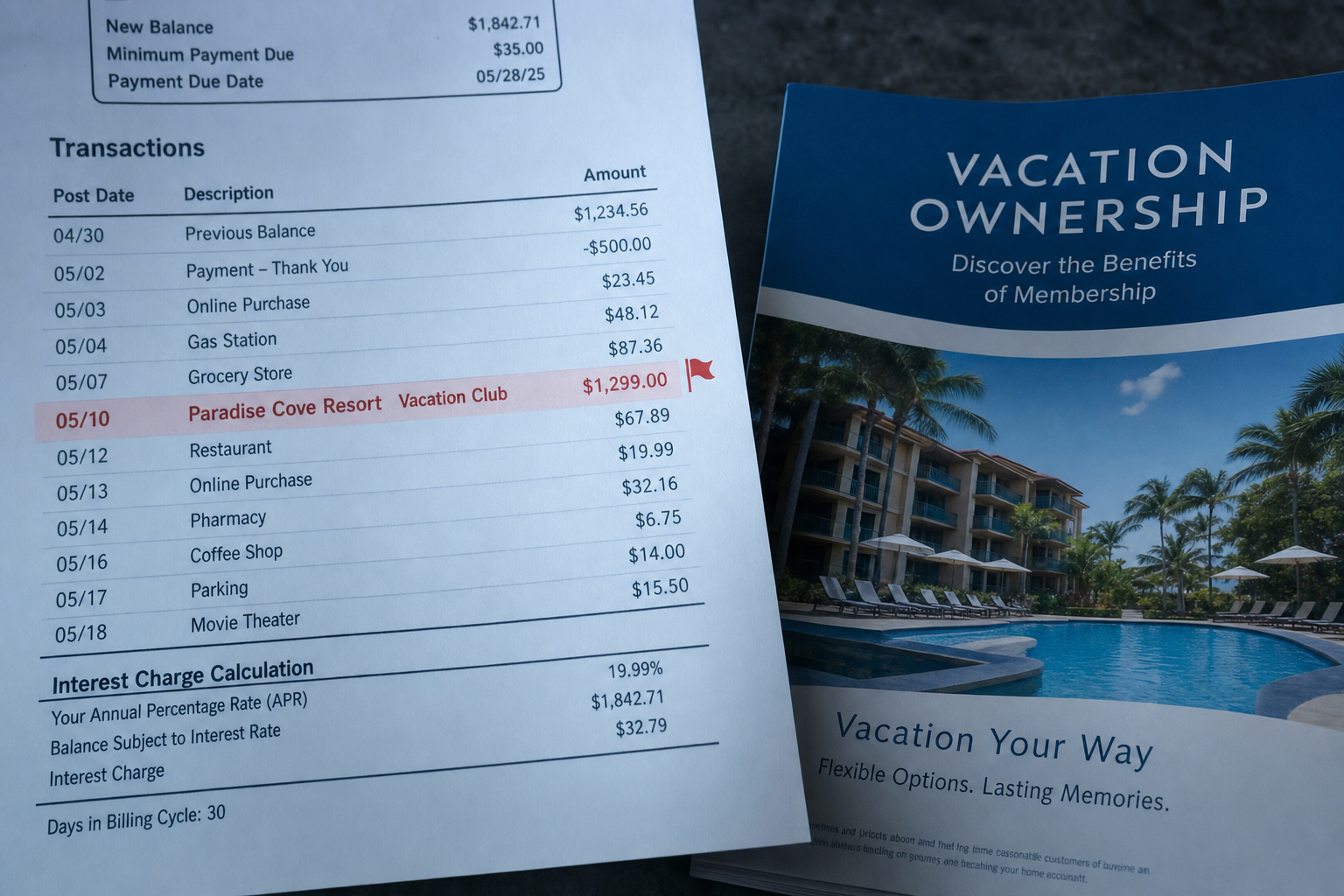

Months 1–3: The resort sends past-due notices. Late fees start accruing — typically 10–18% APR on the unpaid balance. You'll get phone calls, letters, and emails from the resort's accounts receivable team. Some developers (Wyndham, Marriott) keep it relatively professional. Others (Westgate is the most aggressive) use high-pressure collection tactics from day one.

Months 3–6: The account is referred to internal collections or a third-party collection agency. This is when the credit reporting starts. The unpaid balance gets reported as delinquent to all three credit bureaus. Expect a credit score drop of 60–120 points at this stage — the bigger the unpaid balance, the bigger the hit.

Months 6–12: The collection effort intensifies. You'll receive demand letters from collection attorneys. Some developers file civil lawsuits during this window, particularly in states with deficiency judgment laws like Florida, Nevada, and South Carolina. The credit damage continues to compound as fees keep accruing on a contract you're not paying.

Months 12–18: The developer initiates foreclosure (for deeded timeshares) or formal contract termination (for right-to-use and points contracts). Foreclosure adds another major hit to your credit — typically another 100+ points on top of the delinquency damage. The foreclosure itself stays on your credit report for seven years.

After foreclosure: In states that allow it, the developer can pursue a deficiency judgment for the difference between what you owed and what the resort recovered through foreclosure. These judgments can be collected through wage garnishment, bank levies, or property liens in the states that allow those remedies.

The Real Cost of Walking Away in 2026

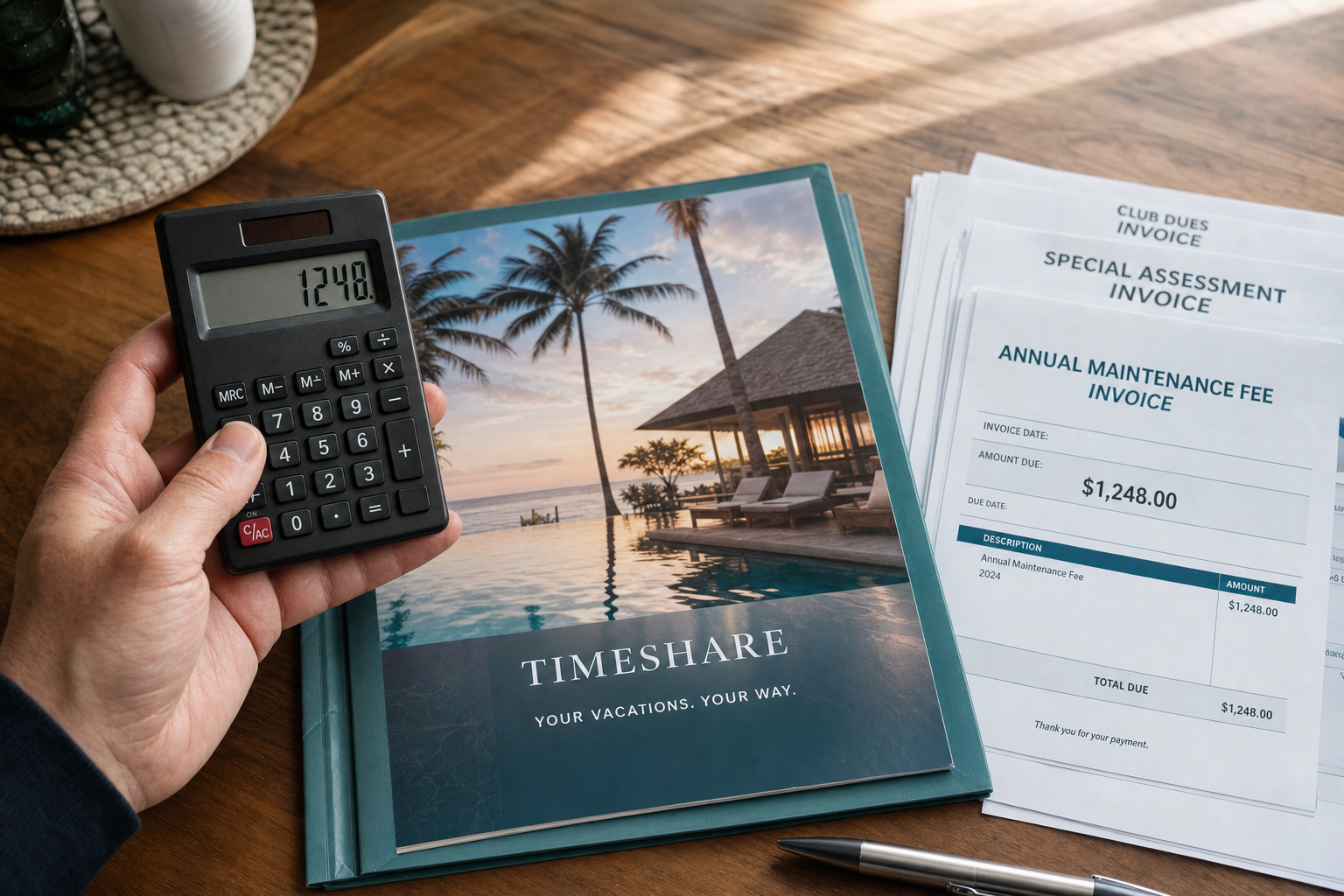

Let's run the numbers on a typical scenario. Owner bought a deeded week in 2015 for $22,000. Annual maintenance fee in 2026 is $1,480 (the current industry average per ARDA's 2025 report). They decide to stop paying.

Over the 18 months from delinquency to foreclosure:

- Unpaid maintenance fees: ~$2,200

- Late fees and interest: ~$400

- Collection costs added: ~$600

- Total balance reported to credit bureaus: ~$3,200

- Credit score impact: 150–200 points

- Foreclosure on credit report: 7 years

- Potential deficiency judgment (in applicable states): $3,200 + attorney fees

For an owner with otherwise good credit (720+), that's the difference between qualifying for a mortgage refinance at 6.5% and being stuck at 9%+ subprime rates. Over a 30-year mortgage on a $400,000 home, that gap is worth roughly $130,000 in additional interest.

The fee you were trying to avoid was $1,480 a year. The cost of walking away from it cleanly without a legal exit can be 80 times that.

When Stopping Payment Actually Makes Sense

There are scenarios where strategic default is the right call. They're narrower than most owners think, but they exist:

Your credit is already damaged. If your credit score is already below 620 from other delinquencies, the marginal damage from a timeshare foreclosure is much smaller. The cost-benefit shifts.

You have no plans to borrow money for 7+ years. No mortgage, no car loan, no business financing, no major credit applications. If you're 70+ years old and own your home outright, the 7-year credit hit is largely theoretical.

Your state doesn't allow deficiency judgments on timeshares. California, Texas, and several others limit or prohibit deficiency judgments after foreclosure. If you're in one of those states, the worst case is foreclosure and credit damage — not a lawsuit and wage garnishment.

The contract is right-to-use, not deeded, and expires within 5 years. Some older right-to-use contracts have natural expiration dates. If you're close enough that the contract will end on its own, the math sometimes works in favor of just riding it out without paying.

You've been refused by every other exit option. Developer rejected your deed-back. Resale market won't take it. Exit companies have looked at your case and said the legal grounds aren't there. At that point, foreclosure may be the only path out.

For everyone else — which is most owners — stopping payment is the most expensive way to solve a problem that has cheaper solutions.

The 4 Legal Alternatives That Don't Wreck Your Credit

1. Developer Deed-Back / Surrender Programs

Wyndham (Ovation), Marriott Vacation Club (Authorized Resale), Hilton Grand Vacations (Resale and Deed-Back), and most other major developers have internal programs to take contracts back from owners. Requirements are usually:

- Loan paid off in full

- Maintenance fees current

- No outstanding special assessments

Acceptance is not guaranteed — developers reject owners they think can be pressured into keeping the contract — but the cost is $0 to $500. If you qualify and they accept you, this is by far the cheapest path. Apply before you stop paying, because they will not take back a delinquent account.

2. Negotiated Settlement Through a Licensed Exit Company

If the developer rejected your deed-back request, or if you don't qualify because of an outstanding loan, a licensed exit company can negotiate directly with the developer's legal team. This costs $3,000–$10,000, takes 6–18 months, and preserves your credit because the contract is formally terminated through legal channels — not breached.

This is the path most owners outside the rescission window end up taking. It's not free, but compared to the $130,000+ long-term cost of damaged credit, the math works.

3. Legal Cancellation Based on Misrepresentation

If your timeshare was sold with false promises — that maintenance fees "wouldn't go up much," that you could "rent it out for income," that it was "a good investment" — you may have grounds for legal cancellation. This is the slowest path (12–24 months) but often the most effective when the sales presentation was aggressive.

4. Sale or Transfer (For Premium Properties Only)

If you own a Disney Vacation Club contract, a Marriott deeded week at a premier resort, or a Hilton Grand Vacations Club property in a high-demand location, the resale market may actually work. Disney DVC contracts typically resell for 60–80% of original purchase price. Marriott premier weeks hold meaningful value.

For the other 95% of timeshares, resale is a dead end and any company telling you otherwise is running a scam.

What to Do Right Now If You Can't Afford the Next Payment

If the bill is due and you genuinely can't pay it, here's the order of operations:

1. Don't ignore it. Ignoring the bill is the worst option because it skips straight to collection without giving you a chance to explore alternatives. Call the resort and ask about hardship deferrals. Most major developers have them, and a 90-day deferral buys you time to set up a real exit.

2. Apply to the developer's deed-back program immediately. Even if you don't qualify, the application creates a paper trail that documents you tried the no-cost option first. This matters if you end up pursuing legal cancellation later.

3. Get a free consultation on your actual exit options. Most exit companies — including ours — offer a no-cost contract review. The review tells you which legal path fits your specific contract before you commit to any strategy.

4. Keep paying while you set up the exit. This is the single most important rule. Stopping payments mid-exit triggers the credit damage cascade and gives the developer grounds to reject any negotiation. Stay current until the exit is formally finalized in writing.

Start with a free, no-pressure consultation →

Frequently Asked Questions

Can the timeshare company sue me if I stop paying? Yes, in most states. Florida, Nevada, South Carolina, Tennessee, and several others actively pursue deficiency judgments after foreclosure. California, Texas, and some others limit this. Even in states that limit judgments, the developer can report the unpaid debt to credit bureaus and refer it to collections.

How long before they foreclose on my timeshare? Typically 12 to 18 months from the first missed payment. Some developers move faster (Westgate has foreclosed in as little as 8 months); others move slower (Wyndham often takes 18–24 months). The contract's specific language and your state's foreclosure laws determine the timeline.

Will stopping payments cancel my timeshare contract? No. The contract remains active until the developer formally forecloses (for deeded timeshares) or terminates the contract (for right-to-use and points). During the months between your last payment and the formal termination, maintenance fees keep accruing as a debt against you — and that debt gets reported to credit bureaus.

How much will my credit score drop if I stop paying? Expect a 60–120 point drop within the first 6 months from delinquency reporting, and another 100+ points if the account proceeds to foreclosure. Total typical impact: 150–250 points, depending on your starting score. The foreclosure stays on your credit report for 7 years.

Can I be jailed for not paying my timeshare? No. Failure to pay a contract debt is a civil matter, not a criminal one. You cannot be arrested or jailed for stopping payments on a timeshare. The consequences are financial (credit damage, collections, potential lawsuits) — not criminal.

Is it legal to stop paying my timeshare maintenance fees? Stopping payment is technically a breach of contract, not a crime. The developer's recourse is civil: collections, credit reporting, foreclosure, and (in some states) deficiency lawsuits. It's a legal option in the sense that you won't be arrested, but it has significant financial consequences.

What if I'm a senior on a fixed income and can't afford the fees anymore? This is one of the most common scenarios in the industry. Many developers have unpublicized hardship programs for seniors — call and specifically ask. If the developer won't help, legal cancellation pathways exist specifically for owners on fixed incomes who can no longer afford the rising fees.

Can my heirs refuse to take over my timeshare if I pass away? In most states, yes. Heirs can disclaim an inherited timeshare, but the process must be completed within a specific window (typically 9 months) and follow proper legal procedures. The safer option is to cancel the contract during your lifetime so there's nothing for your heirs to inherit or disclaim.

The Bottom Line

Stopping timeshare maintenance fees is legal — you won't be arrested, and you won't go to jail. But it's not a clean exit. The contract stays alive for 12 to 18 months while fees keep accruing, your credit takes a 150–250 point hit, and depending on your state, you could face a deficiency judgment for the unpaid balance.

For owners with otherwise good credit, retirement plans that involve borrowing money, or any need to apply for credit in the next seven years, the cost of walking away usually dwarfs the cost of a proper legal cancellation. The cancellation route takes longer and costs more upfront, but it ends the contract permanently without the credit damage.

If you're at the point of considering whether to stop paying, that's the conversation worth having before you make the call. See how a real exit process works, read what other trapped owners experienced, and understand why Axe My Timeshare exists as an independent advocacy resource.

Get your free consultation → or call (949) 731-6607 to talk to a real person about your specific contract.