Paid a Timeshare Resale Scam? Here's Exactly What to Do Next

Paid a Timeshare Resale Scam? Here's Exactly What to Do Next

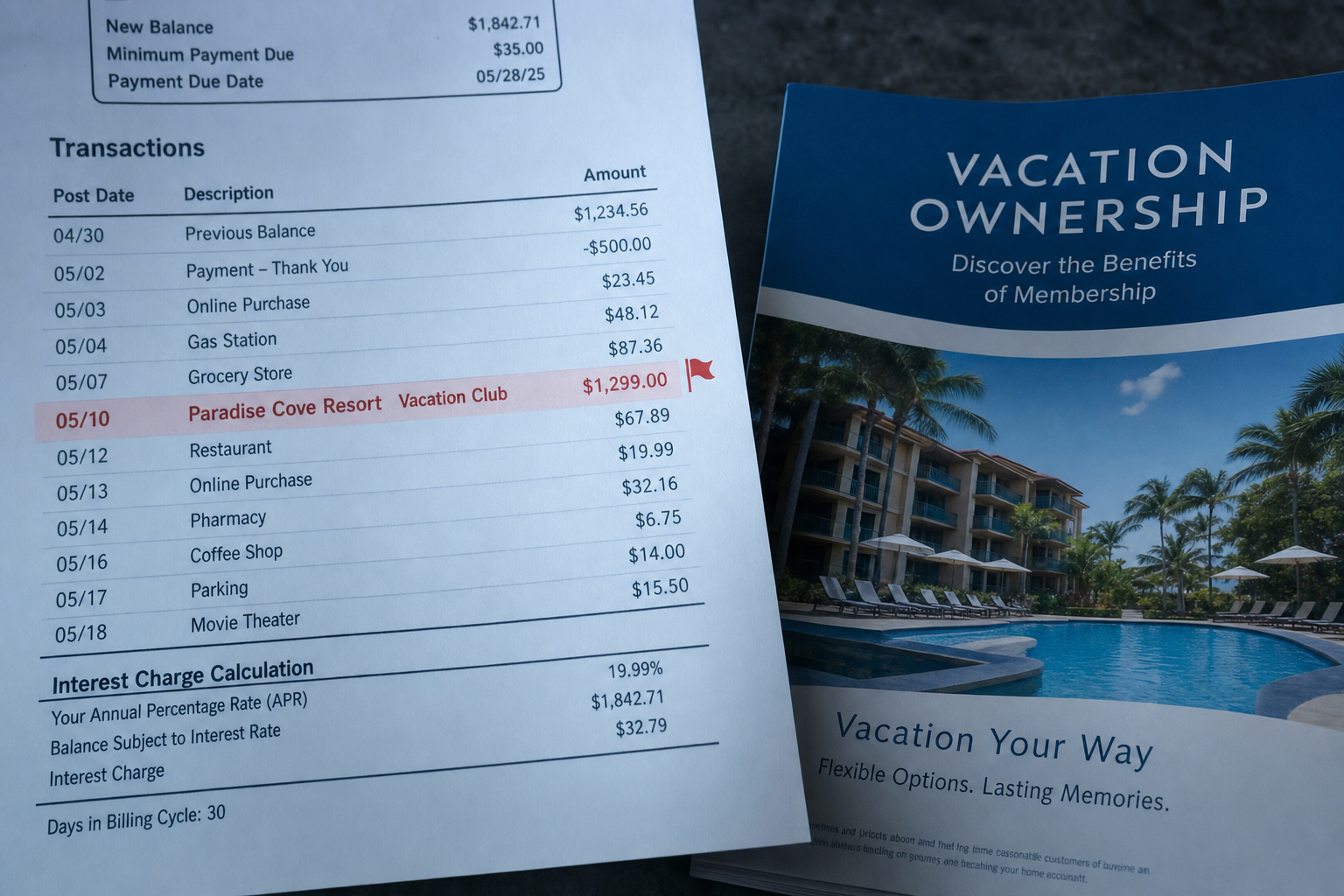

You found what looked like a way out. A company called — or you found them online — and they promised they had buyers ready for your timeshare. You paid an upfront fee. Maybe $500, maybe $3,000, maybe more. Then the delays started. Then the calls stopped getting returned. Then nothing.

You've been scammed. And you're not alone — the Federal Trade Commission receives tens of thousands of timeshare fraud complaints every year, and the FBI tracks timeshare fraud as a priority consumer crime category that disproportionately targets older adults.

What happens next matters more than what already happened. This post walks you through exactly what to do in the days and weeks after a timeshare resale scam — how to attempt to recover your money, how to report the fraud to the right agencies, and critically, how to protect yourself from the follow-on scam that almost always comes next.

What Is the First Thing to Do After a Timeshare Resale Scam?

Stop all further payments immediately.

This sounds obvious, but it isn't always. Scam operations are skilled at manufacturing reasons why one more payment will finally close the deal — a title issue, a tax clearance, a legal hold. The FTC's consumer guidance on refund and recovery scams is explicit: if you've already paid and nothing has been delivered, additional payments will not change the outcome. They will only increase your total loss.

Once you've stopped payment, gather everything: the company name and any doing-business-as names they used, phone numbers and email addresses they contacted you from, every receipt, contract, email, and text in the conversation, and the exact dates and amounts of every payment you made. You will need this documentation for every step that follows.

Can You Get Your Money Back From a Timeshare Resale Scam?

Recovery is possible in some cases — but it depends heavily on how you paid and how quickly you act.

If you paid by credit card, you have the strongest option available: a chargeback under the Fair Credit Billing Act. The law allows you to dispute charges for services not delivered as agreed. The FTC's guide to disputing credit and debit card charges covers the mechanics — but the critical detail is timing. Under federal law, credit card billing errors must be disputed in writing within 60 days of the statement date on which the charge first appeared. If you are still inside that window, contact your card issuer today.

Do not wait.

When you call, use the phrase "services not rendered" or "services not delivered as agreed." Be prepared to provide the documentation you gathered: the contract, any communications, the date you paid, and what was promised. Your card issuer will open a dispute investigation; the merchant (the scam company) then has a window to respond. Many of these operations either cannot respond or choose not to, and the chargeback is resolved in your favor.

If you paid by wire transfer, your options narrow significantly. Wire transfers are the payment method scammers prefer precisely because they are difficult to reverse. Contact your bank immediately after discovering the fraud — if the wire is recent enough (sometimes same-day), your bank may be able to place a hold or recall request before the funds clear on the receiving end. The longer you wait, the less likely this works.

If you paid by check, contact your bank about a stop payment if the check hasn't cleared. If it has, the path to recovery shifts to the complaint and legal channels below.

If you paid by gift card, cryptocurrency, or payment app such as Venmo or Zelle, recovery is very unlikely through the payment channel. These are the methods scammers specifically request when they want to make transactions untraceable. Your focus should shift entirely to reporting.

Where Do You Report a Timeshare Resale Scam?

Report to every relevant agency. Each filing serves a different function, and collectively they build the paper trail that enables enforcement actions.

The FTC at ReportFraud.ftc.gov. This is your primary filing. The FTC feeds complaints into the Consumer Sentinel Network, a database accessible to thousands of law enforcement agencies at the federal, state, and international levels. Your report alone will not trigger a refund — but it contributes to the pattern matching that allows the FTC to pursue enforcement cases. The $140 million judgment against timeshare exit scammer Christopher Carroll grew out of exactly this kind of accumulated complaint data.

The FBI at IC3.gov. The FBI's Internet Crime Complaint Center specifically tracks timeshare fraud and the reload fraud operations that follow initial scams. File a report even if the fraud originated via phone rather than online — IC3 accepts all forms of timeshare fraud.

Your state attorney general's consumer protection office. The National Association of Attorneys General maintains a directory of every state AG office. File a complaint in your home state and in the state where the scam company claimed to be located — if you can identify it. State AGs have direct enforcement authority and have won significant judgments against timeshare fraud operations. The Minnesota AG secured nearly $270,000 in refunds for residents in 2025 from three exit companies specifically. The New Jersey AG won a $10 million judgment against a timeshare resale operation. These cases frequently originate with consumer complaints.

The Better Business Bureau at bbb.org. The BBB has limited enforcement authority but does maintain public complaint records. A formal complaint can occasionally prompt a response from companies that still care about their public rating — and it adds a publicly searchable record that protects future victims.

The Consumer Financial Protection Bureau at consumerfinance.gov/complaint. If your payment involved financing, a credit card issuer, or a debit transaction through your bank, the CFPB has jurisdiction and can apply pressure on the financial institution involved.

What Is Reload Fraud and Why Should You Expect to Be Targeted Again?

This is the section most recovery guides skip — and it may be the most important thing you read today.

After a timeshare resale scam, your information gets sold.

Scam operations maintain what the FTC calls "sucker lists" — databases of people who have already paid a fraudulent company, including your name, contact information, the type of scam that worked on you, and how much you paid. These lists are bought and sold between criminal operations. The FTC's refund and recovery scams advisory documents this pattern explicitly: people who have been scammed once are disproportionately targeted again, because they have demonstrated willingness to pay and established that their timeshare situation is unresolved.

The follow-on contact typically takes one of two forms.

The first is a "recovery company" — someone who calls claiming they can get your money back from the original scammer. They will know details about the original scam, which lends false credibility. They will ask for an upfront fee to begin the recovery process. This is reload fraud: a second scam layered on top of the first one. No legitimate recovery service charges upfront fees to recover fraud losses.

The second form is a "government impersonator" — a caller claiming to be from the FTC, the IRS, or another federal agency, telling you that a settlement has been reached with the company that defrauded you, and that you need to pay a processing fee or provide your bank account number to receive your portion. The real FTC never calls consumers to demand payment or collect personal information over the phone.

If you receive either type of contact after being scammed: hang up, do not provide any information, and report the new contact to the FTC and FBI using the same filing channels listed above. Tell them explicitly that this appears to be reload fraud following an earlier timeshare resale scam.

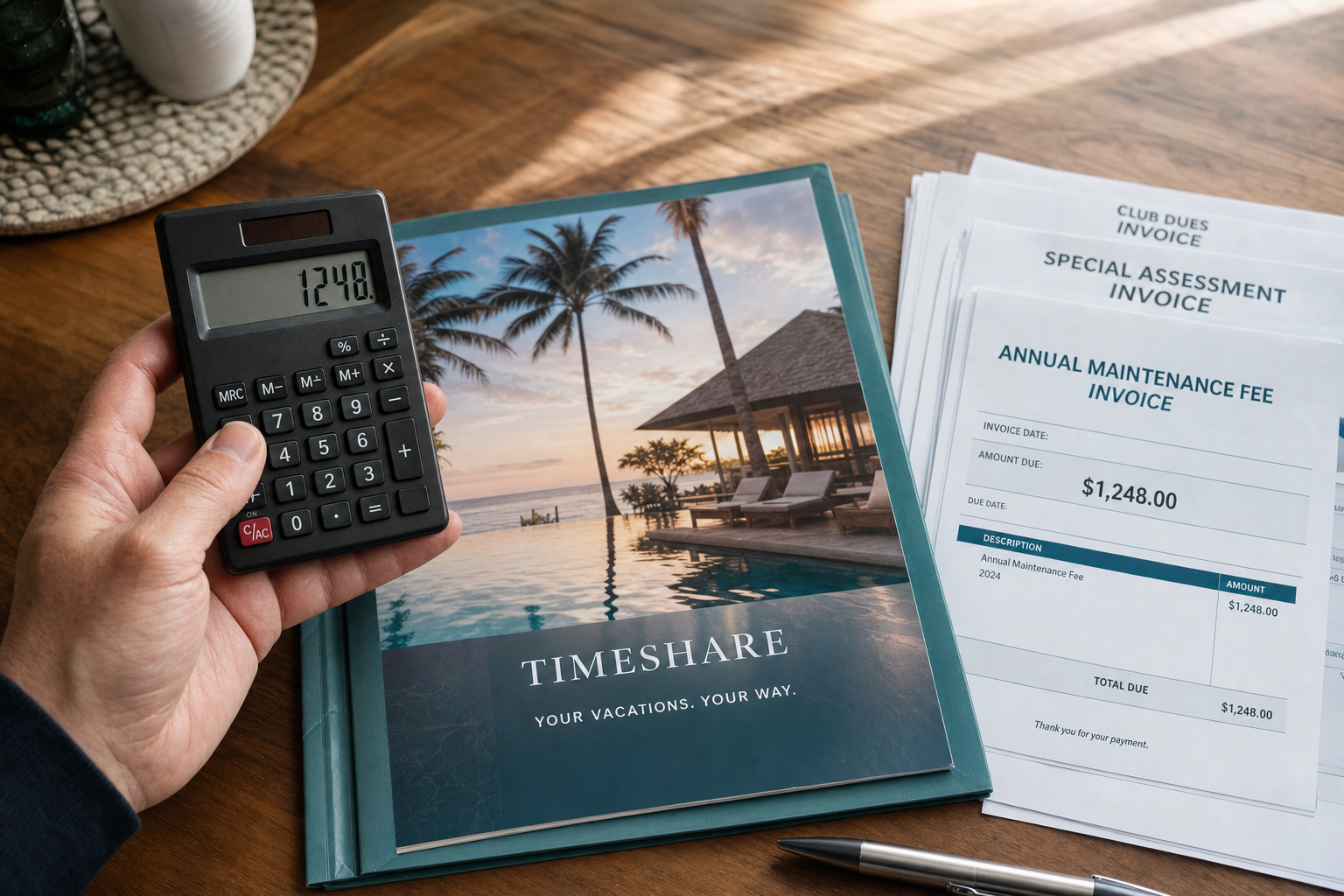

What Happens to Your Timeshare Contract After the Scam?

The scam didn't change anything about your underlying contract. You still own the timeshare. You still owe the maintenance fees. The resort has no knowledge of and no obligation related to what the fraudulent resale company promised you.

This is the part that stings most — you're out the money you paid the scammer and you still have the same problem you started with.

The options for actually resolving your timeshare contract haven't changed. They've never involved resale companies that charge upfront fees. The real pathways — resort deed-back programs, negotiated cancellations through legitimate exit companies, and legal rescission for recent purchasers — exist independently of anything the scam company promised. If your rescission window is still open, read our guide on the timeshare rescission period immediately, as the window is short and the process is time-sensitive. For owners past the rescission period, the complete legal exit guide for 2026 covers every pathway available to you by contract type.

One important note if you're considering a timeshare exit company after being burned by a resale scam: the exit industry has its own bad actors. Our breakdown of what the FTC's $140 million judgment means for timeshare owners covers exactly what the red flags look like inside exit operations — the Carroll case is a precise roadmap of what to avoid. Read it before committing to anyone.

How Do You Protect Yourself Going Forward?

A few practices that directly reduce your exposure:

Register on the National Do Not Call Registry at donotcall.gov. It won't stop scammers who deliberately violate the law, but it eliminates legitimate marketers from the pool and makes unsolicited calls easier to identify as suspicious.

Never act on an inbound call about your timeshare. If a caller claims to have a buyer, a settlement, or a recovery opportunity related to your timeshare, the call itself is the red flag. Legitimate buyers don't cold-call. Legitimate exit companies don't open with a buyer claim. End the call and, if you want to follow up, independently look up and dial the company yourself — do not use a number the caller provides.

Verify before you engage anything. Before paying anyone anything related to your timeshare, look up the company independently, check their BBB complaint history, search their name alongside the words "scam" or "complaint," and verify any claimed real estate license through the state licensing board in the state where your property is located.

If someone asks for wire transfer, gift cards, cryptocurrency, or a payment app — stop. These payment methods are requested specifically to prevent chargebacks and make funds untraceable. No legitimate professional in any field requires payment through these channels.

Frequently Asked Questions

How long do I have to dispute a credit card charge from a timeshare scam?

Under the

Fair Credit Billing Act, you have 60 days from the date the charge first appeared on a billing statement to dispute it in writing with your card issuer. This window is strict — do not delay. Contact your issuer by phone first to get the dispute started, then follow up in writing with your documentation.

Will the FTC refund my money after I file a complaint?

Filing a complaint does not guarantee individual refund. The FTC contributes complaint data to enforcement investigations, and when cases are settled or judged, consumer redress funds are distributed to identified victims. If the company that defrauded you is later the subject of an FTC enforcement action, you may be included in a distribution — but this is not guaranteed and can take years. Your fastest potential recovery path is the credit card chargeback if you paid that way.

Can I sue the timeshare resale company directly?

Potentially, yes. Many state consumer protection statutes allow private civil claims against fraudulent businesses, with the possibility of recovering actual damages, punitive damages, and attorney's fees in some jurisdictions. The statute of limitations for such claims typically ranges from three to five years depending on your state and the type of claim. An attorney who handles consumer fraud matters can assess your specific situation. Do not contact a "timeshare attorney" who called you unsolicited — that is almost certainly reload fraud.

What if the company that scammed me has already shut down?

Scam operations frequently close and reopen under different names, which is why state AG and FTC complaints are important even when recovery seems unlikely. The principals behind these operations are tracked across corporate filings. Additionally, if the operation processed payments through a financial institution, there may be avenues through your bank or card issuer that don't depend on the company still being in business.

Is the company that just called to help me recover my losses legitimate?

Almost certainly not. Legitimate recovery services do not cold-call victims. Any company that contacts you unsolicited claiming to help recover timeshare fraud losses, and then asks for an upfront fee, is running reload fraud. Report them to the FTC at ReportFraud.ftc.gov and to IC3.gov immediately.

→ Get a Free, No-Pressure Consultation About Your Timeshare Contract