Unauthorized Timeshare Credit Card Accounts: How to Spot Them and Fight Back

Unauthorized Timeshare Credit Card Accounts: How to Spot Them and Fight Back

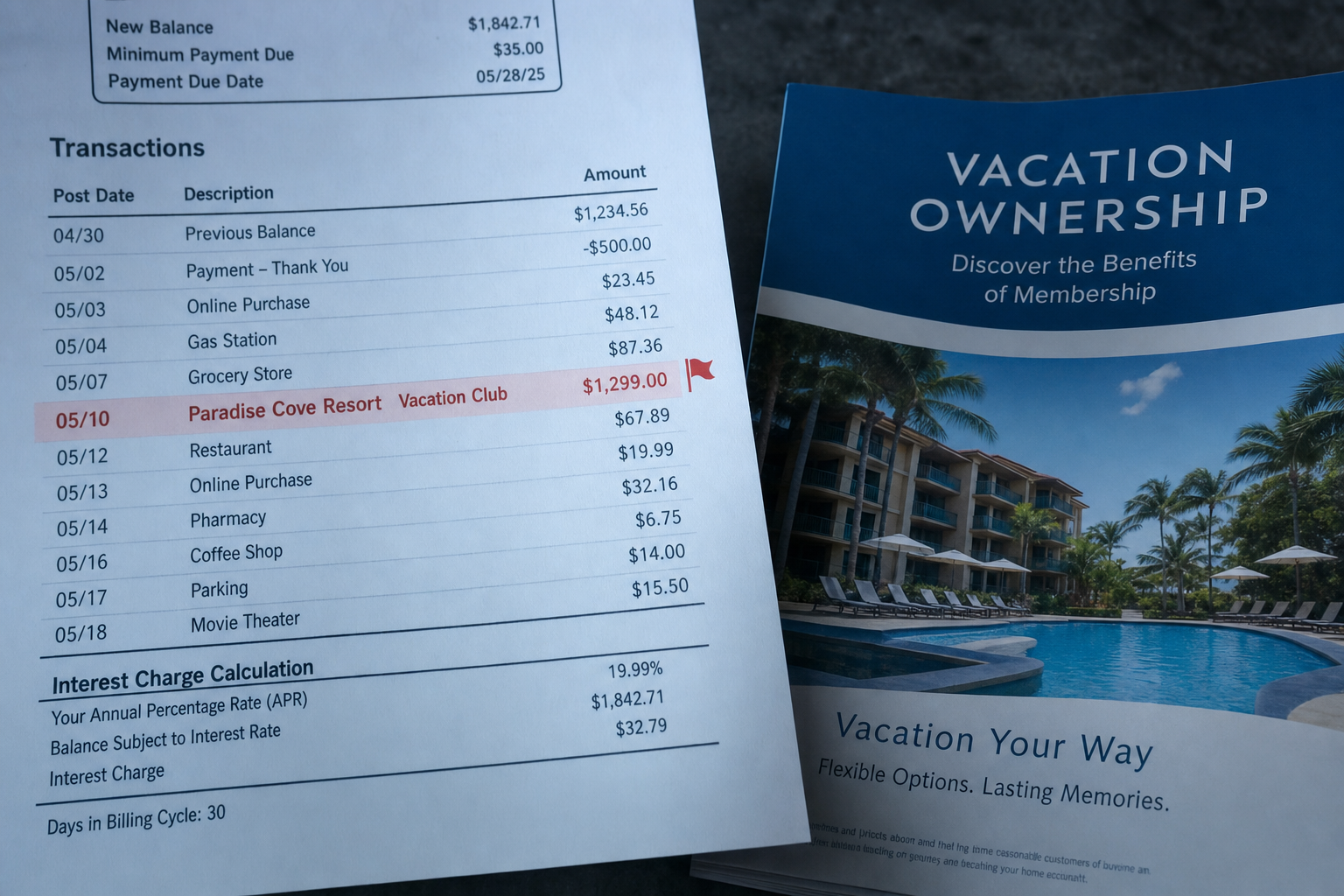

Escalating maintenance fees are frustrating enough. But a growing number of timeshare owners are discovering something worse: a credit card account they never knowingly opened, tied directly to their timeshare purchase — sometimes only found when unexpected charges show up or a new card arrives in the mail.

How Do Unauthorized Timeshare Credit Accounts Actually Happen?

The pattern typically starts inside the sales presentation itself. Timeshare salespeople request personal details — often framed as necessary for documentation or to qualify for a promotion — including Social Security numbers and driver's license information. That data can then be used to open a credit account tied to a co-branded rewards card, sometimes without the buyer's clear, informed consent. Because sales teams frequently operate under account-opening targets and incentives, the pressure to generate new accounts can outweigh the diligence that should go into confirming genuine consent.

Why Do Credit Card Issuers Sometimes Miss This?

Credit card issuers aren't necessarily complicit, but their verification processes weren't built to catch this specific pattern. When a salesperson has a buyer's complete personal information — full name, Social Security number, driver's license — that's often enough to pass an issuer's standard checks, even if the buyer never intended to open a new account. It's a structural gap: the issuer sees a legitimate-looking application; the buyer sees a card they never asked for. This is exactly why consumer vigilance matters as much as institutional oversight — closely guarding personal information during any high-pressure sales environment is one of the few controls a buyer has over this risk before it happens.

How Do You Know If You Have an Unauthorized Account?

A few signals are worth watching for after any timeshare presentation or purchase:

- A credit card arrives that you don't remember applying for.

- Unexplained charges appear tied to a timeshare-branded rewards program.

- A hard inquiry shows up on your credit report from a card issuer you didn't apply to directly.

- A new account appears with a credit limit you never discussed or authorized.

What Should You Do If You Find an Unauthorized Account?

A few concrete, sequential steps make the biggest difference in resolving this cleanly:

1. Notify the credit card issuer's fraud department immediately. A documented account of what happened — including the timeshare presentation where your information was collected — can trigger an internal investigation, and in many cases leads to cancellation of the account and removal of associated debt.

2. File a complaint with the Federal Trade Commission. The FTC accepts complaints related to identity theft and financial fraud, and a filed complaint can help build a pattern of evidence against a specific timeshare company or sales office if others have experienced the same issue.

3. File a complaint with your state Attorney General's consumer protection division. State-level complaints can trigger investigations independent of federal action, and many states have specifically pursued timeshare companies over deceptive sales practices before.

4. Pull your credit reports and dispute the account. Under the Fair Credit Reporting Act, you're entitled to a free copy of your credit report annually from each of the three major bureaus — Equifax, Experian, and TransUnion. Review each one for the unauthorized account and any related hard inquiries, and formally dispute anything that doesn't reflect an account you knowingly opened.

5. Consider a fraud alert or credit freeze. If your personal information was collected during a presentation and you're concerned about further misuse, a fraud alert (free, lasts one year) or a full credit freeze adds a layer of protection against additional unauthorized accounts.

Does This Happen at Major Timeshare Developers, or Just Smaller Operators?

Co-branded credit programs tied to vacation ownership exist across the industry, including at large, well-known developers like Marriott Vacation Club, Wyndham Destinations, and Hilton Grand Vacations. The existence of a legitimate co-branded card program at a major resort brand doesn't mean every account opened through it was properly authorized — the same verification gap can occur regardless of the developer's size or reputation, which is why checking your credit report after any timeshare purchase or upgrade is worth doing no matter which brand you're dealing with.

What If This Is Part of a Larger Pattern With Your Timeshare?

An unauthorized credit account is rarely the only issue in situations like this — it often surfaces alongside broader concerns about how a timeshare was sold in the first place. If you're now dealing with an unauthorized account tied to a Marriott timeshare exit, trying to cancel a Wyndham timeshare, or untangling a Hilton Grand Vacations contract that came with financial surprises you never agreed to, understanding exactly what you own is the starting point for addressing both the credit issue and the underlying contract together.

Frequently Asked Questions

Can a timeshare company really open a credit card in my name without clear consent?

It happens more often than most buyers expect, typically when personal information collected during a sales presentation is used to complete a credit application the buyer didn't clearly understand or agree to.

Will disputing an unauthorized account hurt my credit score?

No — disputing a genuinely unauthorized account is the correct step to protect your credit. Leaving it unresolved is what causes lasting damage, since unpaid charges and hard inquiries you didn't authorize can lower your score over time.

How do I get a free copy of my credit report to check for unauthorized accounts?

Federal law entitles you to a free credit report annually from each of the three major bureaus — Equifax, Experian, and TransUnion — which is the fastest way to spot an unauthorized timeshare-related account.

Is filing an FTC complaint worth it if my individual case seems small?

Yes. Individual complaints contribute to a broader pattern the FTC and state regulators use to identify and act against companies with repeated deceptive practices, even if a single complaint doesn't resolve your case directly.

Dealing With an Unauthorized Account on Top of a Timeshare You Want Out Of?

You shouldn't have to fight a credit card dispute and a bad timeshare contract on your own. Call AxeMyTimeshare at (949) 731-6607 for a free consultation, or visit axemytimeshare.com to see what a structured exit could look like for your situation.